Introduction

Somalia, nestled in the Horn of Africa and echoing with tales of its vibrant diaspora, stands as a beacon of untapped potential in the global financial arena. Historically, Somalia has been a confluence of trade, culture, and migration, and these elements have collectively contributed to a dynamic financial ecosystem, especially within the banking sector. The Somali diaspora, spread across continents, has maintained deep-rooted connections with their homeland. These ties manifest financially as well, with an impressive inflow estimated at 2 million annually. Such substantial remittances underscore the indispensable role of Somalia’s banking infrastructure, which not only manages these funds but also channels them into developmental projects, spurring economic growth and stability. Additionally, the Somali banking landscape is distinctively characterized by its alignment with Islamic principles.

Aerial view of Mogadishu city

Robust Remittance Channels: The continuous inflow from the diaspora provides a steady source of funds, ensuring liquidity in the banking system.

Cultural Affinity: The preference for Islamic banking resonates with the cultural and religious beliefs of the Somali populace, ensuring widespread acceptance and trust in the system.

Economic Renaissance: Post-conflict Somalia is witnessing a phase of reconstruction and development, necessitating robust financial mechanisms to support infrastructural and entrepreneurial ventures.

Strategic Location: Somalia’s strategic position along the East African coast makes it a potential hub for regional trade and finance, further amplifying the role of banks in facilitating cross-border commerce.

As Somalia embarks on this transformative journey, it’s vital to recognize the interplay of its rich history, the unwavering support of its diaspora, and its commitment to Islamic banking principles. These elements not only shape its present but will also profoundly influence its future in the global financial landscape. With a potent mix of cultural depth, strategic positioning, and economic potential, Somalia’s banking sector is poised to be a beacon for investors and institutions alike, offering opportunities that blend tradition with modernity. As we delve deeper into this report, we will uncover the intricacies, challenges, and prospects that define Somalia’s unique banking narrative.

The Evolution of Islamic Banking: A Global Phenomenon with Deep Roots in Somalia

In the wake of the unrestrained 2008 financial crisis, the global financial landscape underwent a paradigm shift. Traditional banking systems, once perceived as unassailable, revealed their vulnerabilities. Amidst this backdrop, Islamic finance emerged as a beacon of stability and resilience. Unlike conventional banking systems, which primarily rely on interest-based operations, Islamic finance emphasizes risk-sharing, asset-backed transactions, and ethical investment principles. These attributes, rooted in centuries-old Islamic teachings, provided a robust alternative to the volatility-ridden conventional systems.

Major global financial institutions, in a bid to diversify and mitigate risks, began to explore the world of Islamic finance. It wasn’t long before they established specialized departments dedicated exclusively to this realm, colloquially termed as the “Islamic window”. These windows weren’t mere tokenistic gestures but robust divisions offering a gamut of financial products aligning with Shariah principles.

While the Western financial hubs were gradually waking up to the potential of Islamic banking, this trend resonated deeply in regions with a predominant Muslim population. Somalia, a nation with rich Islamic heritage, was no exception. The country didn’t just adopt Islamic banking in response to global trends but embraced it as a reflection of its cultural and religious ethos. In Somalia, Islamic banking wasn’t a mere alternative; it was the norm. Most banks, whether large institutions or local entities, practiced Islamic banking, making it an intrinsic part of the nation’s financial fabric.

However, Somalia’s journey with Islamic banking has been distinctive. While the principles of Islamic finance are universally consistent, Somalia’s banking system is characterized by its fragility and less regulated nature. The nation, having experienced prolonged periods of political instability and economic challenges, has a banking framework that’s still in its nascent stages. The regulatory mechanisms, while evolving, have yet to reach the robustness witnessed in more mature Islamic banking markets.

In essence, Somalia stands at a unique crossroad. On one hand, it has a banking system deeply rooted in Islamic principles, resonating with the beliefs of its people. On the other, it grapples with challenges stemming from a less regulated and fragile financial infrastructure. As Somalia continues its journey of economic reconstruction, the evolution and strengthening of its Islamic banking system will undoubtedly play a pivotal role.

Banking Dynamics in Somalia: Trends, Risks, and Opportunities

The Somali banking sector has undergone notable transformations, influenced by an array of factors, from global economic conditions to localized market dynamics and evolving risk perceptions.

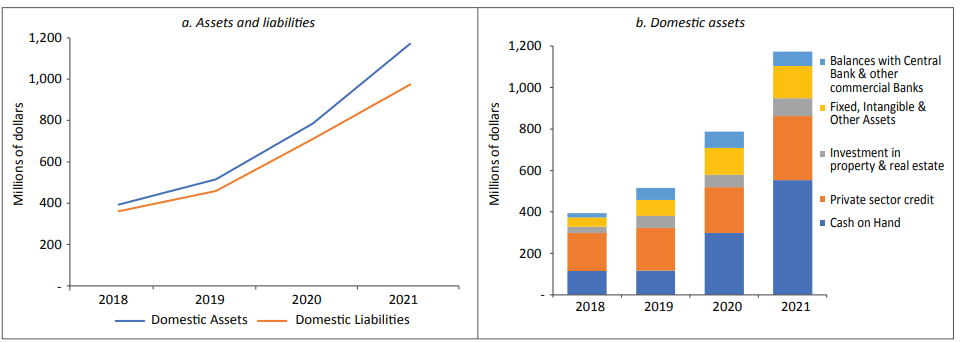

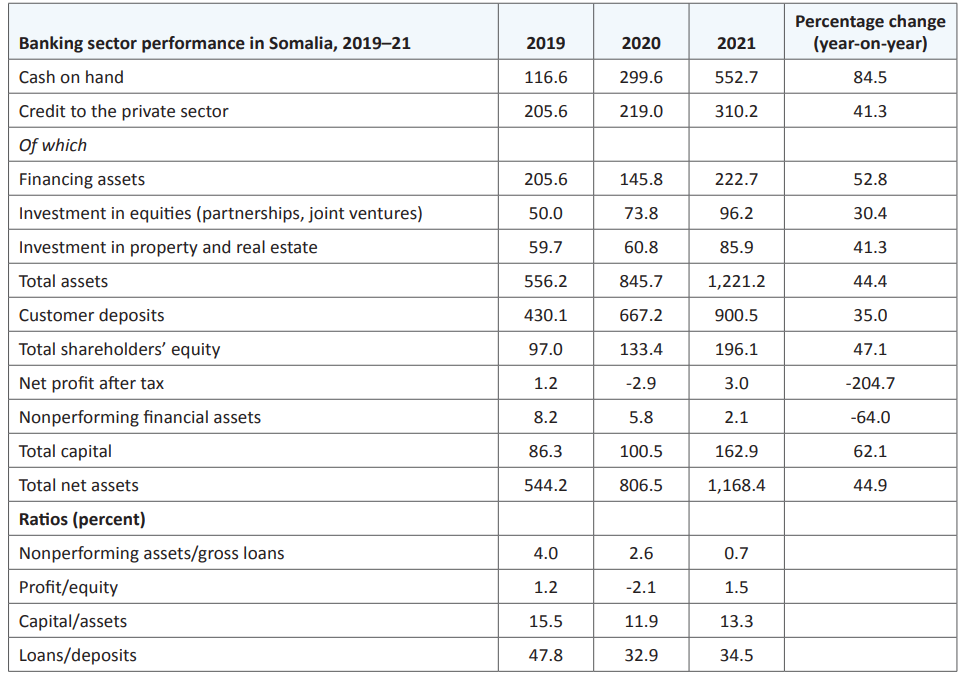

In recent years, commercial banks in Somalia have exhibited a decline in their credit provision to the private sector as a proportion of total assets. This figure dropped from 26.0% in 2020 to 25.4% in 2021. One of the primary drivers for this trend has been an enhanced perception of default risk, largely attributed to the uncertainties brought about by the pandemic. As a consequence, banks have been more reserved, scaling down their outreach and lending activities.

Figure 1 The domestic assets and liabilities of commercial banks in Somalia

Source: central Bank of Somalia

Source: central Bank of Somalia

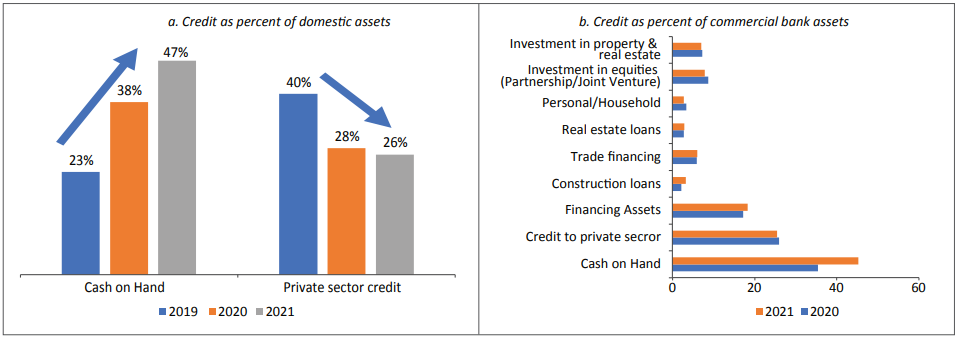

The figure 2 shows that composition of the banks’ loan portfolios has also seen shifts. Personal loans, which once constituted 3.4% of total assets in 2020, shrank to 2.7% in 2021. Similarly, Islamic finance instruments, such as Musharakah (partnership) and Mudarabah (joint venture) loans, retreated from 8.7% of total assets to 7.9%. In stark contrast, the construction sector saw an uptick in loans, with its share growing from 2.1% in 2020 to 3.2% in 2021 as shown in Figure 1.

Interestingly, a pronounced trend among banks has been their preference for liquidity over lending. Many have chosen to keep substantial cash reserves instead of disbursing it as loans to potential borrowers. This behavior resulted in cash on hand surging to 45% of total assets in 2021, a marked increase from 35% in the previous year. Such a trend underscores the prevalent challenges related to finance accessibility in Somalia. Supporting this notion, a 2021 survey revealed a significant financing gap, with about 63% of firms finding it challenging to access credit.

Figure 2 The share of credit going to the private sector

Source: central Bank of Somalia

Yet, amidst this cautious lending environment, the asset quality of commercial banks in Somalia remains praiseworthy. The ratio of nonperforming loans to total loans has been on a decline, suggesting that banks are less at risk from potential loan defaults. This positive indicator, combined with the robust capital asset ratios of these banks, signals that they possess a strong buffer to absorb losses without teetering on the brink of insolvency.

Table 1 Selected indicators of commercial banks performance

Licensing, New Entrants, and the Awaited Commencement

In an era marked by rapid globalization and economic integration, the Central Bank of Somalia despite its current vulnerabilities and not yet fulfilling all traditional roles, it has been active in its efforts to invigorate the nation’s financial landscape. “Acknowledging the rising significance and stability of Islamic banking in international financial arenas, and its deep alignment with Somali traditions and values, the Central Bank has taken decisive steps to diversify the nation’s banking landscape,” stated the Central Bank.

However, while the licensing phase has been successfully executed, these banks are on the threshold of their operational journey in Somalia. They have yet to commence their full-fledged operations within the country. The anticipation is palpable, as the entry of these licensed banks is expected to usher in a new era of financial innovation, competition, and enhanced services tailored to the unique needs of the Somali populace.

Central Bank Headquarters in Mogadishu

The Participation Banking Paradigm: A Deep Dive into Ziraat Katlim’s Model

At the heart of modern Islamic banking lies the ‘Participation Banking Model,’ a system that is intrinsically different from its conventional counterparts. Ziraat Katlim, in its operational ethos, epitomizes this model, bringing to the fore a fresh approach to banking that is both ethical and aligned with the core principles of Islamic finance.

Unlike traditional banks where the emphasis is often on interest-based transactions, participation banks like Ziraat Katlim center around mutual benefit and risk-sharing. This approach is manifest in how they raise funds. Special accounts, known as ‘current’ and ‘participation’ accounts, become the primary vehicles for accumulating capital. These aren’t just namesakes but signify the collaborative nature of the banking process, where both the bank and its customers participate in a shared financial journey.

A cornerstone of this model is its unwavering commitment to interest-free financing. Every financial product or service offered by Ziraat Katlim adheres stringently to this principle, ensuring that both the earnings and the benefits are distributed without the influence of interest, making the entire process more transparent and just.

Central Bank Headquarters in Mogadishu

Risk, an inevitable aspect of any financial endeavor, is approached differently in the participation banking model. Instead of placing the onus of risk solely on the investor or the borrower, the model advocates for a shared responsibility. This means that both the capital owner (often the depositor or investor) and the labor (which could be an entrepreneur or business entity) collaboratively shoulder the risk. Such an approach not only distributes the potential burden but also fosters a sense of collective responsibility and mutual trust.

Ziraat Katlim’s Comprehensive Financial Offerings: Meeting the Needs of Somalians

In the dynamic landscape of modern banking, the services offered by financial institutions play a pivotal role in determining their relevance and appeal to customers. Ziraat Katlim, with its profound understanding of the Somali market, has meticulously crafted a suite of financial services that are not just aligned with Islamic principles but are also tailored to meet the unique needs and aspirations of Somalians.

- Cash Financing & Corporate Financing Support: Recognizing the entrepreneurial spirit of Somalians and the growth of local businesses, Ziraat Katlim offers specialized financing solutions. These empower businesses to procure essential goods, from raw materials to finished products, facilitating seamless operations and growth. With competitive profit rates, businesses find this offering both attractive and crucial for their expansion endeavors.

- Installment Trade Financing: The diverse needs of businesses, ranging from acquiring machinery to vehicles and other infrastructural essentials, are addressed through this tailored financing solution. Ziraat Katlim’s deep-rooted understanding of the Somali market ensures that such financial products are both accessible and beneficial for local enterprises.

- Foreign Exchange Financing: In an increasingly globalized world, where cross-border transactions are commonplace, this innovative product shields customers from exchange rate volatilities. It ensures that Somalians, whether businesses or individuals, can engage in international trade with predictability and confidence.

- Financial Leasing: Offering flexibility to businesses, financial leasing allows the use of an asset for most of its economic life, with an option to assume ownership subsequently. This is particularly beneficial for startups and established businesses in Somalia looking to optimize their capital expenditure.

- Investment and Treasury Products: For Somalians seeking ethical investment avenues, Ziraat Katlim offers participation funds. These funds invest in a diversified portfolio, ensuring compliance with Islamic principles and offering investors a chance to grow their wealth ethically.

- Trade Financings: Ziraat Katlim understands the importance of trade for Somalia. With specialized products like export and import financing, traders are ensured smooth and hassle-free cross-border transactions, fostering the nation’s trade potential.

Somalia, with its rich history and strategic location, has always been a hub for trade, culture, and commerce. As the nation undergoes economic reconstruction and development, there’s a palpable need for robust financial services that understand and cater to the unique requirements of its people. Ziraat Katlim, with its comprehensive suite of offerings, not only fills this gap but also plays a vital role in propelling Somalia towards a brighter economic future. The bank stands as a testament to what is possible when financial expertise converges with a deep understanding of local needs.

The Somali Financial Landscape: A Tapestry of Potential and Challenges

Somalia, a nation steeped in history and marked by its resilience, presents a mosaic of opportunities and hurdles in its banking landscape. As the country navigates its path of economic reconstruction, the role of its banking sector becomes increasingly pivotal, acting as the linchpin for sustainable growth and development.

The potential of Somalia’s banking sector is undeniable. With a young, aspirational population, a strategic geographical location, and a diaspora that remains deeply connected to its roots, there’s a burgeoning demand for sophisticated financial services. However, juxtaposed against this potential are the challenges that have historically marred the sector.

The current banking infrastructure in Somalia can be characterized as nascent and fragile. While there are local banks striving to cater to the population’s needs, the absence of significant international banking players is palpable. This gap means that the nation misses out on the advanced financial products, technological innovations, and expertise that global banks often bring to the markets they operate in.

Yet, in what can be termed as a testament to Somalia’s indomitable spirit, the financial ecosystem continues to thrive. A significant portion of this resilience can be attributed to the immense inflow of funds into the country. Remarkably, nearly 60% of Somalia’s national budget is anchored by donations. When one factors in the additional funds channeled for disaster relief, humanitarian aid, and developmental projects, the scale and importance of these financial inflows become profoundly evident. These funds not only bolster the country’s economy but also underscore the global community’s commitment to Somalia’s resurgence.

An interesting facet of the Somali market is its cosmopolitan nature. Despite its challenges, Somalia attracts a myriad of professionals and entities from across the globe. From experts contributing to infrastructure projects to the peacekeeping, the presence of non-Somali nationals is significant. This diverse demographic, with its unique financial needs, particularly international banking services, further underscores the demand and potential for a robust banking sector.

In essence, while the road ahead for Somalia’s banking sector is dotted with challenges, the journey promises rewards for those willing to innovate, understand the local nuances, and contribute to the nation’s overarching vision of economic revival.

The Somali(sed) Banking System: A Unique Model with Inherent Challenges

In the vast spectrum of global banking systems, Somalia’s “Somali(sed) system” stands out as a distinctive model, deeply rooted in the nation’s cultural and societal nuances. This system, while reflecting the trust-based ethos of Somali society, presents a paradigm that is markedly different from conventional banking practices witnessed globally.

At the heart of the Somali(sed) system is the emphasis on communal trust and shared responsibility. Unlike many global systems where government identification often suffices to access banking services, Somalia’s model demands a more layered approach to customer verification. Prospective customers must not only provide their government identification but also bring forth a guarantor and offer collateral. This tri-layered approach, while enhancing the trust quotient, ensures that both the bank and the customer are anchored in a mutual bond of responsibility and accountability

However, the uniqueness of the Somali(sed) system also brings with it challenges, particularly for banks unfamiliar with its intricacies. Banks that are new entrants to the Somali market, accustomed to more streamlined customer onboarding processes, often find the Somali(sed) system complicated. The demands for guarantors and collaterals, while culturally resonant, pose operational challenges and can act as deterrents for banks aiming to cater to the broader retail market. The hesitancy to adapt can sometimes translate into missed opportunities, both for the banks and the Somali populace seeking diverse financial services.

Expanding Financial Frontiers: The Indispensable Role of an Effective Central Ban

In the dynamic world of banking, regulatory oversight acts as the bedrock ensuring stability, trust, and fairness. In Somalia, this critical responsibility rests with the Central Bank, which stands as the sentinel overseeing the operations of commercial banks within its jurisdiction.

The Central Bank doesn’t just play a supervisory role; it actively shapes the direction of the nation’s banking sector. One of its significant mandates could be the endorsement of the Islamic banking model. Given the cultural and religious alignment of the majority of Somalians towards Islamic principles, such a mandate would not be out of place. If the Central Bank were to advocate this model, commercial banks operating in the region would have no choice but to comply. This potential directive underscores the profound influence and authority the regulatory body wields in shaping Somalia’s banking landscape.

However, with great power comes immense responsibility. The Central Bank’s decisions, while steering the banking sector’s course, must be balanced, ensuring that they foster growth, inclusivity, and innovation while upholding the principles of fairness and stability.

Conclusion: Navigating the Horizon of Somali Banking

Somalia, a nation at the crossroads of history and modernity, stands poised for a transformative journey in its banking sector. As we reflect on the intricacies, challenges, and potential of this landscape, it becomes evident that the linchpin for sustainable growth and success is, undoubtedly, customer satisfaction.

In an era marked by rapid technological advancements and shifting customer expectations, the essence of banking remains unchanged: to serve the needs of the people. For Somali banks, this means not just offering financial products but tailoring them to resonate with the unique cultural, social, and economic nuances of the nation. If banks can adeptly navigate this balance, ensuring that their services are both effective and efficient, the road ahead is paved with promise. A satisfied customer is not only loyal but also becomes an advocate, propelling the bank’s reputation and reach in the community.

However, while customer-centricity is the keystone, the broader architecture of the banking sector demands collaborative efforts. Regulators, including the Central Bank of Somalia, and financial institutions must foster a symbiotic relationship. This partnership should be anchored in mutual respect, shared vision, and open dialogue. As the sector stands on the cusp of evolution, aligning with international best practices becomes imperative. This alignment not only enhances the sector’s credibility on the global stage but also ensures that the Somali populace benefits from the latest innovations and robust financial safeguards.

Yet, in this pursuit of global alignment, it’s crucial that the unique requirements and aspirations of the Somali people remain at the forefront. Blindly replicating international models without contextual adaptations could lead to misaligned offerings and missed opportunities. Therefore, a balanced approach, which marries global best practices with local insights, will be the most fruitful.

Recommendations:

- Strengthen Regulatory Frameworks: While maintaining flexibility, regulators should enhance oversight mechanisms, ensuring transparency, accountability, and stability in the sector.

- Enhance Digital Infrastructure: Embrace technological advancements, fostering digital banking solutions that cater to the younger, tech-savvy demographic while ensuring accessibility for all.

- Cultural Training for New Entrants: Banks unfamiliar with the Somali(sed) system should invest in cultural and operational training, ensuring seamless integration and understanding of local nuances.

- Customer Feedback Mechanisms: Establish robust channels for customers to provide feedback, ensuring that banks remain agile and responsive to evolving needs.

- Collaborative Forums: Create platforms where regulators and financial institutions can engage in constructive dialogues, sharing insights, challenges, and potential solutions.

In essence, the horizon for Somalia’s banking sector is luminous with potential. With concerted efforts, strategic vision, and an unwavering commitment to serving the Somali people, the sector can indeed script a success story that stands as a testament to resilience, innovation, and growth.